Economics

Finance

Policy

Apple supply chain, Atmanirbhar Bharat, battery storage, capital allocation, China manufacturing, Dani Rodrik, deindustrialisation, DPIIT, East Asian economies, Economic Development, economic policy, education spending, Emerging Markets, Energy Transition, export led growth, flying geese model, foreign direct investment, geopolitics, global value chains, import substitution, India, India 2047, India China relations, India economy, India GDP, India Investment, Indian manufacturing, industrial ecosystems, Industrial Policy, Make in India, manufacturing sector, PLI Scheme, Production Linked Incentive, R&D spending, semiconductors, solar manufacturing, supply chain, Trade Policy

AnilMehta

India’s ₹1.91 Lakh Crore Lesson – Why Incentives Alone Cannot Buy an Industrial Revolution

There is one uncomfortable truth: money, by itself, does not build manufacturing ecosystems. It merely reveals whether one exists.

India’s Production Linked Incentive programme, launched in 2020 with genuine ambition to lift manufacturing’s share of GDP from a stagnant 13–14 per cent to 25 per cent, is now old enough to be judged on evidence rather than intent. The verdict is not catastrophic. But it is instructive — and considerably more sobering than official communications suggest.

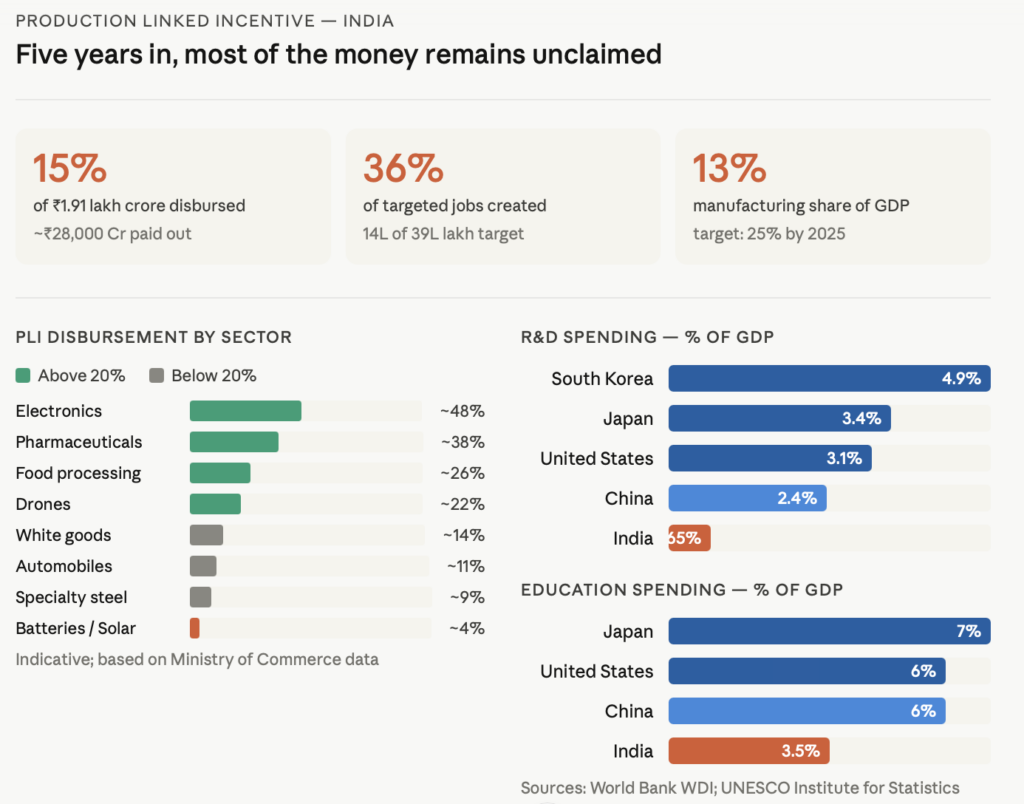

Of the ₹1.91 lakh crore (approximately $23 billion) committed across 14 sectors, barely 15 per cent had been disbursed as of the latest government reporting cycle.¹ Only four sectors — large-scale electronics manufacturing, pharmaceuticals, food processing, and drones — have achieved disbursement rates exceeding 20 per cent.¹ Against a stated target of 39 lakh jobs, approximately 14 lakh have been created.¹ Investment commitments, the one genuine bright spot, have reached roughly 62 per cent of target — respectable, but a long way from translating into the operational milestones that trigger actual incentive payments.

These numbers demand a structural reckoning, not a communications exercise.

The Scheme’s Internal Contradictions

PLI’s design logic is defensible in principle. Link government payouts to production milestones rather than capital deployment alone, thereby rewarding outcomes rather than inputs. In practice, two fault lines have emerged.

The first is structural. Eligibility criteria — particularly minimum bid sizes — have in several sectors filtered out experienced players while admitting well-capitalised but industrially inexperienced conglomerates. The battery storage PLI, requiring a minimum capacity of 5 gigawatt-hours, was ultimately won by three companies, none of whom had prior experience in the sector. When one prospective Chinese technology licensor subsequently withdrew from a critical partnership, the project stalled. This is not an isolated misfortune. It is a predictable consequence of industrial policy that conflates financial scale with technological capability.

The second fault line is more systemic. India remains deeply import-dependent for raw materials, manufacturing equipment, and technical expertise in precisely the sectors PLI seeks to develop. Solar module manufacturing states this with painful clarity. Against a target of 8.7 GW of fully integrated capacity, only approximately 4 GW has been commissioned in five years.¹ In a parliamentary statement, Union Minister Pralhad Joshi acknowledged that the programme depends on imported raw materials, equipment, and expertise — a dependency that makes the incentive structure partly circular.² You cannot achieve the domestic value addition required to claim the incentive without the domestic capability that the incentive was supposed to create.

The Geese That No Longer Fly in Formation

To understand why India finds itself in this bind, one must look beyond scheme design to political economy.

The East Asian economic miracles of the late twentieth century were built on a specific and largely unrepeatable architecture. Kaname Akamatsu’s “flying geese” model — positing a sequential transfer of industries from advanced to developing economies — accurately described what happened across East Asia.³ Japan industrialised, transferred labour-intensive industries to South Korea and Taiwan, which in turn passed them further down the chain. China was the last and largest beneficiary.

But the model’s success depended on something that standard economic accounts tend to understate: deliberate political sponsorship. The United States absorbed Japanese exports through the 1950s and 1960s despite domestic protectionist pressure, provided concessional financing, and transferred technology as part of a Cold War containment strategy. Japan subsequently extended the same architecture toward South Korea and, critically, toward China. Beijing’s accession to the WTO in 2001 — with vigorous American support — and the substantial transfer of US capital and technology that followed were the terminal acts of this long pattern.

India, arriving late to industrialisation in a world that has decisively pivoted from globalisation toward strategic localisation, finds none of this architecture in place. Washington has been explicit: it does not intend to replicate with India the strategic concessions it extended to China over two decades. As one senior US trade official remarked in 2023, the logic that made economic interdependence with China appealing is precisely what policymakers now consider a cautionary tale.⁴

China, meanwhile, has tightened its grip on rare earth minerals and critical material supply chains — the very inputs that underpinned earlier waves of Asian industrialisation. India’s own restrictions on Chinese investment, introduced through Press Note 3 in April 2020, reduced Chinese FDI inflows dramatically. Whether the March 2026 decision to lift those restrictions will meaningfully alter trajectory remains uncertain; bilateral strategic tensions are not resolved by capital account regulations.

Dani Rodrik has established with rigour that latecomer industrialisers face structural headwinds that their predecessors did not.⁵ Automation, the consolidation of global supply chains, and the protective trade policy of advanced economies collectively mean that manufacturing-led convergence is harder — possibly far harder — than it was for Japan or South Korea. India’s challenge is compounded by an additional variable Rodrik’s framework implies but does not always foreground: the absence of a credible external sponsor willing to absorb the adjustment costs of another country’s industrialisation.

The Deeper Deficit

Consider where high-value manufacturing actually resides in the modern global economy. Apple, to take the most studied example, captures an estimated 58 per cent of the iPhone’s total value addition — not through production, but through design, software, and ecosystem control.⁶ The assembly, conducted across supply chains spanning multiple Asian jurisdictions, captures the residual. The implication is stark: the countries competing to host manufacturing capacity are, in a structural sense, competing for a shrinking share of the pie. The high-value nodes — research, design, intellectual property — remain with countries that have built deep research ecosystems over decades.

India’s gross expenditure on research and development stands at approximately 0.65 per cent of GDP.⁷ China’s equivalent figure is approximately 2.4 per cent; South Korea’s exceeds 4 per cent.⁷ India’s public expenditure on education is 3–4 per cent of GDP; Japan allocates close to 7 per cent.⁸ These are not peripheral inputs. They are the determinants of which nodes in the value chain a country can eventually compete for. A country spending less than 1 per cent of GDP on R&D is, almost by definition, not competing for the nodes where value concentrates.

This is not an argument for abandoning manufacturing ambition. Geopolitics has made self-sufficiency in critical sectors — batteries, semiconductors, defence components — a strategic necessity that exists independently of the usual calculus of comparative advantage. Resource weaponisation is no longer an abstract risk; it is current policy. India must build domestic capability in these sectors regardless of whether global markets reward it.

But monetary incentives alone will not build the ecosystem required. What the PLI architecture has revealed is that India has a first-order problem before the second-order problem of incentive design: supply chain depth, technical human capital, and research infrastructure are prerequisites for PLI to function as intended, not outputs it can be expected to generate.

What Sound Policy Requires

The lesson from PLI’s partial performance is not that industrial policy is futile. It is that industrial policy is a complement to institutional capacity, not a substitute for it. Schemes that assume the ecosystem and merely need to accelerate it — as electronics and pharmaceuticals have broadly demonstrated — work reasonably well. Schemes that are asked to conjure the ecosystem into existence against an import-dependent supply chain — as batteries and solar modules have demonstrated — struggle structurally, regardless of the financial envelope.

Three adjustments are consequential. First, eligibility design must weight demonstrated sectoral capability over financial scale. Conglomerates with balance sheets but no domain knowledge will consistently underperform specialist firms, regardless of incentive magnitude.

Second, PLI must be accompanied by complementary investments in the supply chain infrastructure it currently takes as given. Import substitution in components cannot be mandated by the same scheme that is trying to incentivise downstream assembly; the sequencing must be explicit and funded.

Third, and most fundamentally, India must treat R&D and education investment not as medium-term aspirations but as immediate policy emergencies. The gap between India’s research intensity and that of its industrial competitors is not a matter of insufficient ambition. It is a matter of insufficient urgency. Closing it requires a decade of consistent, ring-fenced investment before competitive manufacturing capacity at the high-value end of the spectrum becomes plausible.

India’s PLI experiment is not a failure. It is an incomplete diagnosis followed by a partially calibrated prescription. The country identified that manufacturing needed stimulation. It has not yet fully confronted the prior question: stimulation of what, exactly, and on what foundation?

The difference between a developing economy and a developed one is not, in the end, the generosity of its incentive schemes. It is the depth of its institutional capacity to use them.

References

- Ministry of Commerce and Industry, Government of India (2024). Production Linked Incentive Schemes: Sectoral Progress and Annual Report. New Delhi: Department for Promotion of Industry and Internal Trade (DPIIT).

- Lok Sabha Debates (2024). Statement by Union Minister Pralhad Joshi on Solar Manufacturing Progress under PLI, Ministry of New and Renewable Energy. New Delhi: Parliament of India.

- Akamatsu, K. (1962). A historical pattern of economic growth in developing countries. Journal of Developing Economies, 1(1), 3–25.

- Office of the United States Trade Representative (2023). 2023 Trade Policy Agenda and 2022 Annual Report. Washington D.C.: USTR.

- Rodrik, D. (2016). Premature deindustrialization. Journal of Economic Growth, 21(1), 1–33.

- Kraemer, K. L., Linden, G. & Dedrick, J. (2011). Capturing Value in Global Networks: Apple’s iPad and iPhone. Personal Computing Industry Center (PCIC), University of California, Irvine.

- World Bank (2024). World Development Indicators: Research and Development Expenditure (% of GDP). Washington D.C.: World Bank Group.

- UNESCO Institute for Statistics (2023). Government Expenditure on Education as a Percentage of GDP. Montreal: UNESCO-UIS.