Economics

Finance

Policy

Technology

Adani Defence, Carbon Fibre, China Dependency, Defence Investing, Defence Sector India, Drone Manufacturing, Drone Policy, Drone Stocks India, Drone Technology, Dual Use Technology, Emerging Markets, Fixed Wing Drones, FPV Drones, Geopolitical Risk, geopolitics, Ideaforge, India 2030, India Drones, Indian Defence Industry, Indian Economy, Industrial Policy India, Investment Analysis, Investment Strategy, L&T Defence, Make in India, MALE Drones, Modern Warfare, Operation Sindoor, PLI Scheme, Rare Earth Minerals, Semiconductor Supply Chain, Solar Industries, Strategic Autonomy, Supply Chain Risk, UAV, Ukraine War Drones, VTOL

AnilMehta

India’s Drone Sector’s Uncomfortable Truth

India’s industrial ambitions unfold across five decades — from the License Raj’s cumbersome machinery to the liberalisation of 1991, from the IT services revolution to the current “Make in India” campaigns. Each era carried its own brand of hope, its own supply-side constraints, and its own gap between political vision and economic reality. India’s drone sector, as it stands in 2026, is textbook territory for that particular tension.

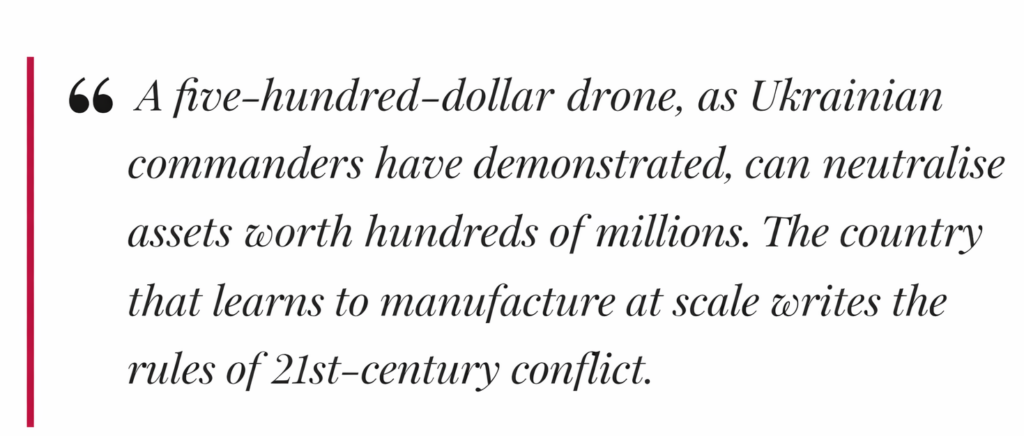

The geopolitical context writes itself. On 28 February this year, the United States struck Iranian targets with drones. Tehran retaliated the very next day with drone salvos across the Middle East. Meanwhile, Ukraine continues to hold the Russian military at bay — not with aircraft carriers or armoured columns, but with a torrent of inexpensive, domestically produced unmanned systems. The lesson has not been lost on New Delhi. A five-hundred-dollar drone, as Ukrainian commanders have demonstrated, can deliver damage measured in the tens of millions. Modern warfare has crossed a threshold, and the arithmetic favours the country that manufactures at scale.

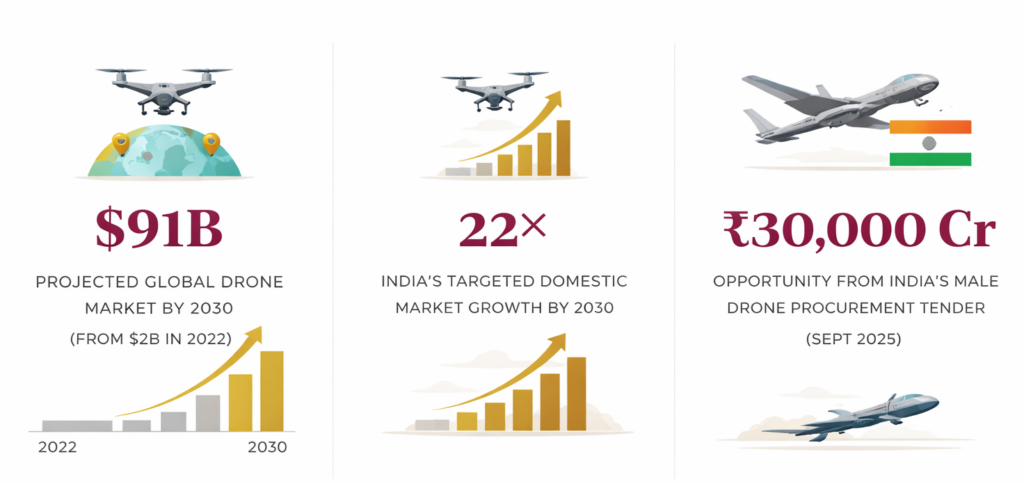

India’s Civil Aviation Ministry believes the country will rank among the world’s three largest drone markets within four years. The numbers are bracing. Today’s domestic market — roughly ₹4,600 crore — is projected to exceed ₹1 lakh crore by 2030, implying an annualised growth rate north of 20 per cent. Industrial houses of the calibre of Adani Enterprises, Larsen & Toubro, Solar Industries and JSW are not dabbling in this sector: they are building manufacturing capacity at scale. The defence establishment, stung by import dependency exposed during the 2020 Galwan clash and subsequent border tensions, has moved with unusual urgency. In September 2025, the armed forces floated tenders for 87 domestically produced Medium Altitude Long Endurance (MALE) drones — a ₹30,000 crore procurement signal that the market could not have missed.

Understanding the Architecture of the Opportunity

To invest wisely in this sector, one must resist the temptation of a monolithic view. Drone businesses are not interchangeable. The first analytical axis is reusability: a surveillance drone deployed on border patrol is a capital asset, maintained over years and generating recurring aftermarket revenue in spare parts, software upgrades, and annual maintenance contracts. A loitering munition — the kamikaze FPV drones that Ukraine has been producing at 200,000 units a month — is ammunition. Its revenue model is purely volumetric, cyclical, and ultimately hostage to the rhythm of conflict. Solar Industries, which entered the consumable drone business through its Nagastra loitering munitions programme and whose products were operationalised during Operation Sindoor, is the archetype of the latter. Its centuries-long legacy in explosives manufacturing provides genuine synergies here, but investors should price in the volatility that comes with a customer base of essentially one — the Ministry of Defence.

The second axis is airframe architecture. Fixed-wing drones, much like conventional aircraft, are energy-efficient, can glide for extended periods and cover vast distances with minimal power. Iran’s Shahed family of munitions, capable of traversing 2,000 to 2,500 kilometres before impact, belongs here. The trade-off is manoeuvrability: a fixed-wing drone cannot hover, making it unsuitable for precision close-quarters operations. Multi-rotor platforms — the quadcopters made familiar by consumer photography and by Rancho’s cinematic contraption in the 2009 Bollywood classic Three Idiots — offer precise hovering and agile directional control, but their continuous motor operation bleeds energy at a punishing rate. They are, for this reason, inherently short-range. Ukraine’s FPV kamikaze drones, effective but limited to front-line engagements, cost roughly $500 apiece. Iran’s fixed-wing Shahed costs forty times as much — and the gap is almost entirely explained by airframe complexity, range capability, and the autonomous targeting systems embedded within.

The fastest-growing category today, and the one drawing the heaviest institutional investment globally, is the VTOL hybrid: aircraft that combine vertical take-off and landing capability with fixed-wing efficiency during cruise. These systems are positioning themselves for long-range logistics, large-area surveillance, and the emerging passenger air mobility segment. Ideaforge Technology — India’s sole pure-play publicly listed drone manufacturer — has operated in VTOL hybrid and multi-rotor configurations for two decades. The company has carved out a genuine niche, but its order book remains lumpy: as high as ₹300 crore when large defence contracts land, and as low as ₹13-14 crore when they do not. That is not a criticism of management; it is the structural reality of a market at an early stage of institutionalisation.

The Supply Chain: Where Ambition Confronts Physics

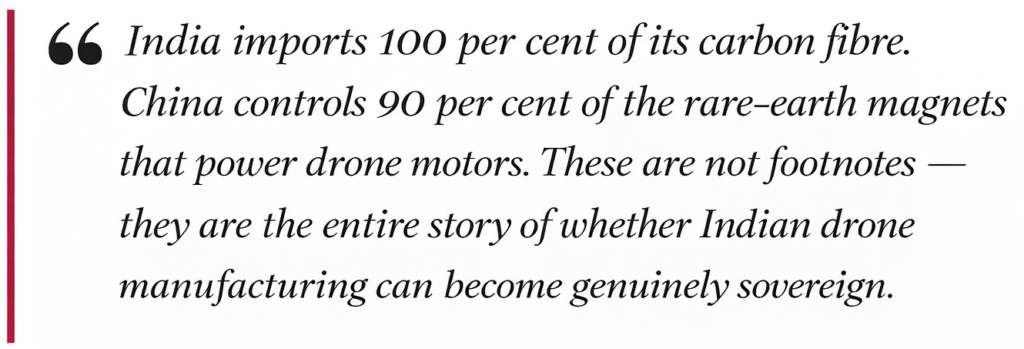

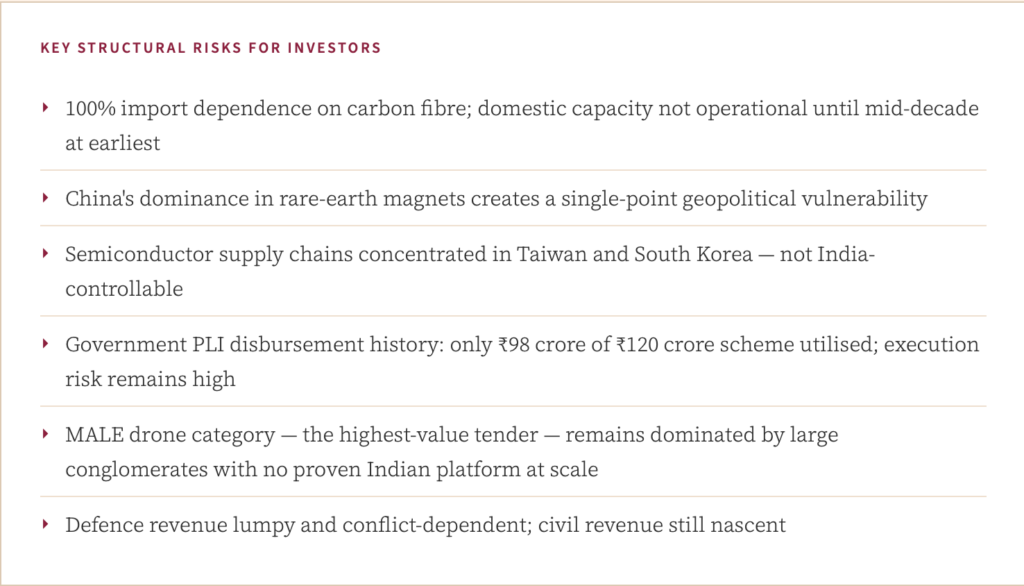

Here is where I must temper the enthusiasm, because in five decades of watching industrial policy I have learned that a nation’s aspirations are only ever as durable as its supply chain. India’s drone manufacturing ecosystem rests on an alarmingly fragile foundation of imported inputs. Carbon fibre — the structural backbone of virtually every advanced airframe — is not produced domestically. India imports the entirety of its carbon fibre requirements from the United States, Japan, France, and Germany. Reliance Industries announced in 2025 that it would build India’s first world-class integrated carbon fibre plant, and the ambition is credible given the conglomerate’s execution track record. But a plant announced is not a plant producing, and the 2030 deadline does not allow for prolonged ramp-up curves.

The propulsion challenge is, if anything, more acute. The permanent magnets that drive drone motors are manufactured from rare-earth elements, and China produces 90 per cent of the world’s rare-earth magnets. This is not an abstraction — it means that every Indian drone that takes flight today does so on the sufferance of Chinese export policy. The battery situation compounds this: China processes two-thirds of the world’s lithium and more than 70 per cent of the graphite used in lithium-ion cells. And at the semiconductor layer — the brains of any autonomous system — India sources over 90 per cent of its chips from Taiwan, China, and South Korea.

The honest assessment is this: until very recently, most Indian drone companies were sophisticated assembly operations. They imported Chinese components, integrated them locally, and sold the result as domestically manufactured product. A 2022 import ban on assembled drones closed that loophole at the system level, but component imports remained permissible and, according to reporting by the Economic Times, some manufacturers still source 70 per cent of their bill of materials from China. Ideaforge has achieved a commendable 60 per cent indigenisation ratio, but even they remain dependent on multiple foreign supply chains for critical inputs.

The Policy Architecture and Its Gaps

The government’s 2021 Production Linked Incentive scheme for drones, valued at ₹120 crore, disbursed only ₹98 crore — a modest utilisation rate that says less about company appetite than about the administrative friction inherent in India’s industrial incentive architecture. A second PLI iteration, reportedly budgeted at ₹1,000 crore, is under discussion. That is a tenfold increase, and if executed with greater administrative agility, it could meaningfully accelerate component localisation. But the honest investor must ask: can India simultaneously develop indigenous carbon fibre production, rare-earth magnet refining, lithium battery cell manufacturing, and semiconductor packaging within a four-year window? The answer, regrettably, is almost certainly no — not at scale, not with the domestic demand for sovereign capabilities that defence procurement requires.

This is not a counsel of despair. India should pursue partial indigenisation aggressively, prioritise supply chain diversification away from China across all critical input categories, and invest heavily in the software and autonomy layers — areas where Indian talent has a demonstrated global edge and where import dependence is far lower. The dual-use thesis is compelling: an estimated 60 to 70 per cent of drone components serve both civil and military applications, which allows companies to spread R&D costs across larger addressable markets. In 2025, 77 per cent of the $3.86 billion in global commercial drone funding went to dual-use companies. The market has already expressed its preference.

The Investment Verdict

For long-horizon institutional investors, the structural case for Indian drone manufacturing is sound. The geopolitical tailwinds are permanent: no government in New Delhi, of any political complexion, will reduce defence procurement or dial back indigenous manufacturing imperatives after the lessons of 2020 and the subsequent years of regional tension. The demand curve — civil and military alike — is real and growing. Companies positioned in higher-complexity categories such as MALE drones and VTOL tactical systems will enjoy substantially better pricing power and entry barriers than those competing in the commoditised small-drone segment, where Chinese manufacturers currently dominate on cost.

However, the sector is early. There are no Indian drone companies that have yet demonstrated the consistent revenue visibility that warrants the valuation multiples sometimes ascribed to them in the current enthusiasm. Supply chain risks are not priced. Execution risk on government incentive programmes is not priced. The dependency on Chinese components — in a sector that exists partly to provide strategic autonomy from China — is a paradox that remains structurally unresolved.

In 1991, India open its economy and observed how a decade passed before the structural reforms translated into the corporate earnings growth that investors had anticipated from year one. The drone sector may follow a similar arc. The vision is right. The ambition is proportionate to the threat environment. But the foundation — materials, components, semiconductors, policy execution — will take longer to build than the promotional literature suggests.

DisclaimerThe analysis contained herein is solely for informational purposes and does not constitute financial, investment, or legal advice. All investment decisions are made at the sole discretion and risk of the reader. The author accepts no liability for any financial outcomes arising from actions taken on the basis of this commentary.