Economics

Finance

Philosophy

Policy

Technology

AI compute, board governance, capital allocation, CEO strategy, China, compliance risk, critical minerals, decoupling, economic statecraft, EV supply chain, export controls, friendshoring, Geopolitical Risk, global capability centres, India, India manufacturing, Industrial Policy, managed fragmentation, national security, pharmaceutical APIs, rare earths, reshoring, selective denial, semiconductors, solar manufacturing, supply chain resilience, technology geopolitics, technology policy, trusted partner, US-China relations

AnilMehta

The boardroom has become the front line of technology geopolitics

The integration of the last three decades was not simply a pattern of trade. It was an order — a set of shared assumptions powerful enough that no firm had to think about them. Design in California, lithography in the Netherlands, fabrication in Taiwan, assembly in the Pearl River Delta, refining in China, packaging in Malaysia: each link sat where it could be done best or cheapest, and the system held because everyone accepted the same premise — that commercial efficiency and national interest pointed in the same direction. Governments policed the rules of exchange but did not dictate the map. Comparative advantage was not a theory we debated; it was the operating system we built on.

That premise is gone. Governments have decided that technology is too important to be left to markets, and in deciding it they have changed the rule itself. The question a board now answers before it sites a plant, signs a supplier or commits capital is no longer where is this most efficient? but where is this most defensible — against sanction, against denial, against a licence that can be revoked? This is not a worse version of the old order. It is a different order, running on a different logic, and most executives are still optimising for a rule-set that no longer governs.

Call the result managed fragmentation. Not decoupling — the scenario that dominates headlines and is almost certainly wrong — but a world in which the chain still spans borders while every border now carries a toll, a licence requirement, or a denial regime.

The chain did not shorten. The principle that organised it inverted.

Because the inversion is in the logic rather than the geography, it does not show up on a map of where things are made; it shows up in the cost, the risk and the legal exposure of making them there. The mistake is to treat this as a forecasting problem for the policy team. It is a governance problem for the chief executive — and it has already rewritten the economics of the firm.

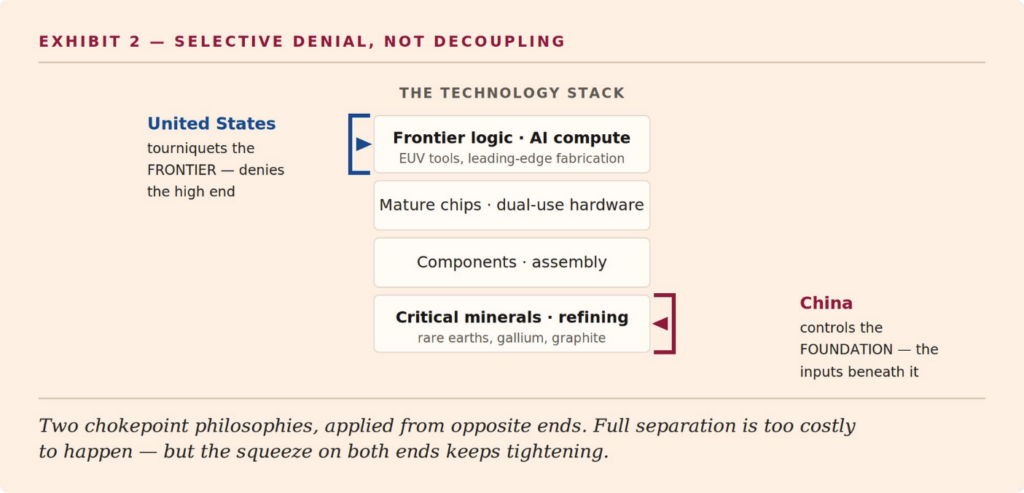

Begin with the contest that frames everything else. The American posture toward China is not a wall; it is a tourniquet applied to specific arteries — frontier logic chips, the equipment that makes them, AI compute, and the dual-use edge. Call it selective denial. Full separation is too expensive for both sides and too disruptive for everyone in between, so it will not happen. But the high end will keep narrowing, and the list of restricted nodes will keep lengthening, because each restriction creates the political appetite for the next. Anyone budgeting on a return to open frontier trade is mispricing the asset.

What too few boardrooms have absorbed is that the response is now symmetrical and institutional. Beijing has stopped improvising. Episodic retaliation — the unofficial customs delay, the quiet boycott — has hardened into law: an unreliable-entity list, an anti-foreign-sanctions statute, export-licensing controls over gallium, germanium, graphite and the rare-earth processing chain that the rest of the world has spent forty years declining to build. For any firm with one foot in the American compliance order and one in the Chinese market, these are no longer political risks to be monitored. They are conflicting legal obligations to be reconciled — and on some days they cannot be.

The cost of all this does not appear where most managers look for it. Duplicate fabs, in-country production mandates, bifurcated data and component lines, localisation rules — none of these are line items a chief financial officer can isolate and cut. They are a structural tax on the enterprise, paid as permanently thinner margins, slower capital cycles and lower asset utilisation. Equity markets have, in my view, not finished repricing this. A generation of valuations was built on the assumption that the most efficient global configuration was also the achievable one. That assumption is now false, and the gap between the efficient chain and the permitted chain is the new cost of doing business.

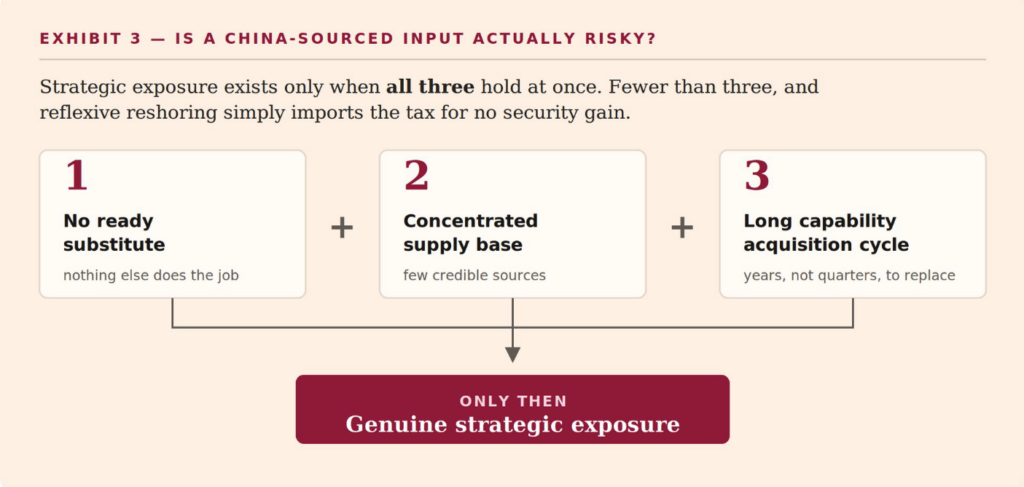

The temptation, having grasped this, is to purge Chinese inputs wholesale. That is a strategic error dressed as prudence. A Chinese-sourced input is dangerous only when three conditions hold at once: it has no ready substitute, it sits in a concentrated supply base, and the time to build the capability elsewhere is measured in years rather than quarters. Where all three are true — certain magnets, precursors, refining steps — you have genuine exposure that warrants real capital. Where they are not, reflexive reshoring simply imports the tax for no security gain. The discipline is to tell the two apart, input by input, rather than to govern by slogan.

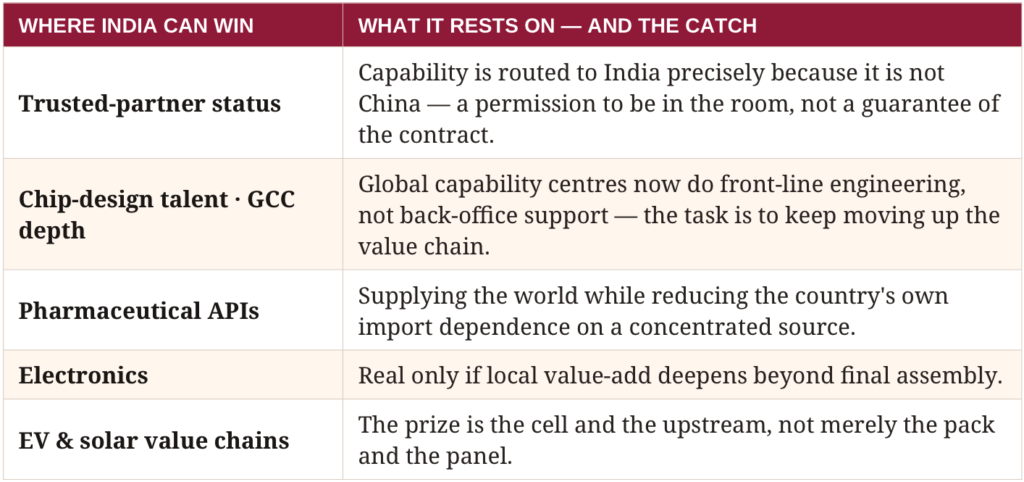

This is where India’s moment is real but widely misunderstood. Trusted-partner status — the willingness of the United States, Japan, Europe and others to route capability into India precisely because it is not China — is the most valuable industrial asset the country has been handed in a generation. It opens doors across a specific set of value chains.

But trust is a permission, not an outcome. It converts into capability only through execution — through plants that actually reach yield, ecosystems that actually deepen, and clearances that actually move. The world is offering India a queue position. Holding it requires delivery, and delivery has been our recurring weakness, not our strength.

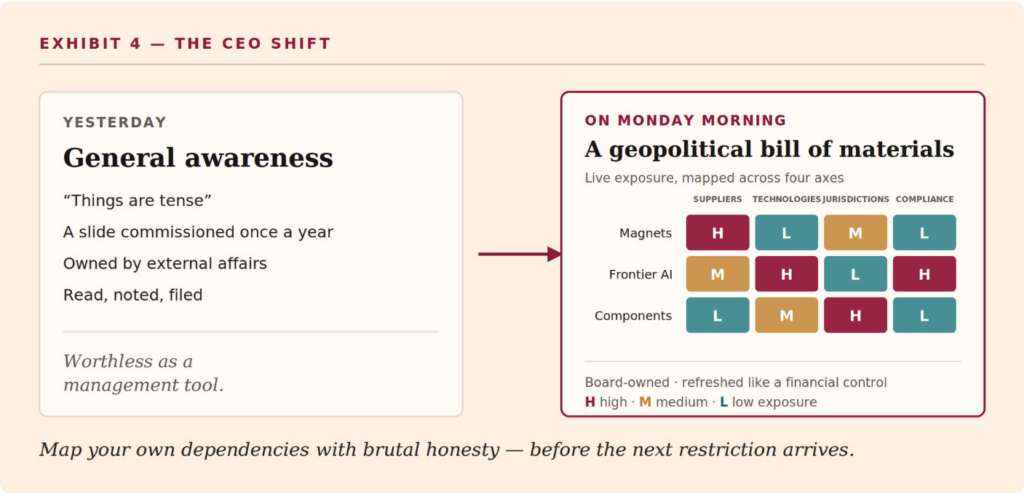

So what should change on Monday morning? The chief executive’s agenda must move from awareness to cartography. General geopolitical literacy — the conference-circuit understanding that things are tense — is now worthless as a management tool. What is required is specific exposure mapping: a live picture of which suppliers, which technologies, which jurisdictions and which compliance obligations create binding risk, and where a single chokepoint could halt a product line. Think of it as a geopolitical bill of materials, owned at board level and refreshed like a financial control — not a slide commissioned once a year from external affairs.

The firms that will compound through this decade are not the ones with the strongest opinions about Washington and Beijing. They are the ones that have mapped their own dependencies with brutal honesty and allocated capital against them before the next restriction arrives. The age in which geopolitics was someone else’s department is over. It now sits on the chief executive’s desk, between the capital plan and the risk register — which is exactly where it belongs.

Note – references to specific Chinese legal instruments (the unreliable-entity list, the anti-foreign-sanctions framework) and to export-licensing controls on gallium, germanium, graphite and rare-earth processing were accurate as of early 2026. This area moves quarterly.